Investment Insights Home Page

The Interest Rate Shakes

March 3, 2021

U.S. 10-year Treasury interest rates have increased over 50% since year-end creating a disruption on the bond market and contributing to a recent slide in equities. We evaluate the causes and implications of this increase, which provide insight to the rhetorical question – When is good news actually bad news?

The U.S. 10-year Treasury interest rate closed the month of February at 1.4% after hitting an intra-day high over 1.6% on February 25th. This rate represents an increase of over 50% since the year-end rate of 0.91%. Domestic equities (S&P 500) sympathetically declined approximately 4% over the past two weeks.

Why are interest rates rising?

Interest rates are rising based on the perception that inflation is set to increase. (inflation is a major determinant in longer-term interest rates.) These expectations are, in turn, a byproduct of an economy that continues to gain steam. So, isn’t this good news? Yes, usually. However, the pace and rate of inflation is the actual concern. As the markets try to figure this out, we get the interest rate shakes – disruptions in bond and equity markets.

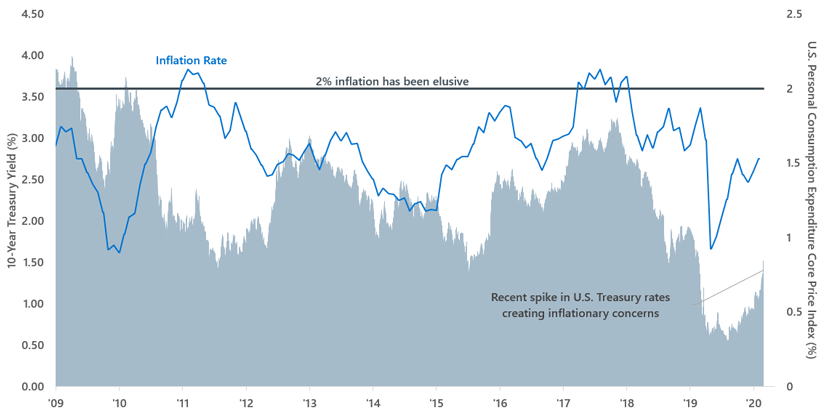

Exhibit: Interest Rate Shakes – Historically, Inflation Has Been Elusive...

Source: Bloomberg. Past performance may not be indicative of future results. Inflation in this chart is defined as the Personal Consumption Expenditure (“PCE”), which is a measure is the component statistic for consumption in gross domestic product (GDP) collected by the United States Bureau of Economic Analysis (BEA). It consists of the actual and imputed expenditures of households and includes data pertaining to durable and non-durable goods and services. It is essentially a measure of goods and services targeted towards individuals and consumed by individuals.

Why has this negatively impacted equities?

Commonly held wisdom suggests that rising inflation/interest rates hurt equities in the sense that equity valuations levels (i.e., Price to Earnings (P/E) ratios) should decline. However, this is somewhat exaggerated in that equity P/Es decline not just on higher interest rates, but also on elevated risks, such as Fed tightening (i.e., increase in Fed Funds rates) or economic weakness. Neither of those risks appear to be an imminent threat.

Regarding Fed tightening, the Federal Reserve is on record stating that they have entered a new era regarding inflation expectations. Historically, they have determined that inflation should be 2%, thereby starting to increase rates prior to those levels. The end result has been that inflation has rarely actually hit and held at the 2% level as seen in the provided exhibit. This also suggests that economic growth could have been stronger if the Fed let inflation climb higher. The new Fed policy entails an “average inflation” targeting at or above 2%. This means they will let inflation run longer and hotter before raising Fed Funds rates in an effort to curb inflation and slow the economy. The end result is a Fed induced economic slowdown is not an imminent threat.

Moreover, positive economic momentum continues. There is no shortage of:

- Fiscal and Monetary Stimulus – global levels are historically unprecedented,

- Global Re-openings - are broadening as vaccinations pick-up and Covid-19 cases roll-over,

- Economic Momentum - continues to build steam globally,

- Domestic Elevated Personal Savings Rates – are expected to rise even more, serving as dry powder for pent-up demand, and

- Consumer Net Worth Levels - are at all-time highs.

These factors and others suggest we are early in a new economic expansion with lots of economic tailwinds.

Portfolio Implications

It is important to note that domestic corporate earnings (i.e., S&P 500) and prices generally peak at the end of expansions. As we appear to be at the beginning of a new economic expansion, this suggests a longer road ahead for equities. While a recent approximate 4% slide in domestic equities is unnerving, it should be considered in the context that the S&P 500 averages 3 to 4 declines per year of over 5%. Interest rates should continue to increase, but risk assets are still currently poised for more gains. Fixed income should continue to be considered for its overall lower risk anchor in portfolios. And, there are still some areas within fixed income that are relatively attractive.

Our investment team continues evaluate and will provide updates as newsworthy events unfold. In the meantime, please contact your CWM Advisor or any member of your CWM wealth advisory team for any additional guidance or answers to any questions you may have.

DEFINITIONS

U.S. 10-Year Treasury: A bond issued by U.S. government for borrowing money; it is widely accepted as a proxy for many other important financial matters, such as mortgage rates.

S&P 500: Widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 9.9 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 3.4 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

P/E Ratio: is the ratio for valuing a company that measures its current share price relative to its per-share earnings.

DISCLOSURE

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Calamos Wealth Management, LLC (“Calamos”), or any non-investment related content, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Calamos is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, personalized investment advice from Calamos.

Please remember that it remains your responsibility to advise Calamos, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.calamos.com.

© 2021 Calamos Wealth Management. All Rights Reserved. Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.

6339_0321_CWM