Investment Insights Home Page

The Ability to Change

February 16, 2022

Identifying the compelling strategies for Fixed Income portfolios to adapt during periods of Rising Interest Rates

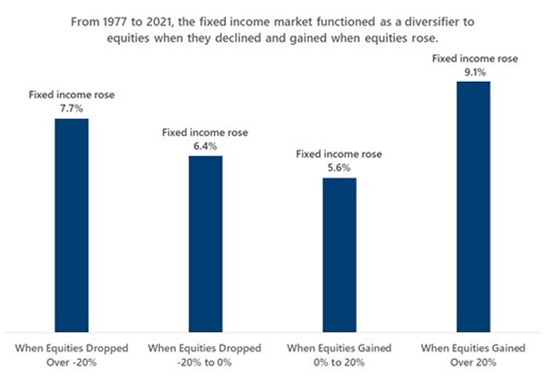

As we all know, investment portfolios should be tailored to meet each investor’s goals and cash-flow needs. For many years, an allocation to equities and traditional fixed income accomplished this goal - equities offered upside participation and fixed income provided cash-flow and a stabilizing mechanism, particularly during periods of sharp stock market declines. In exhibit 1, we highlight this. On average, traditional fixed income gained (U.S. Aggregate Index) 7.7% in years when equities declined 20% or more. When equities had a decline ranging from -20% to 0%, fixed income gained 6.4%. As shown on the right side of the chart, fixed income also had upside participation when the environment was more positive, but as you’d expect, equities tended to outperform.

Exhibit 1: U.S. Investors Show Home Bias despite More Opportunities Elsewhere

Source: Bloomberg. Past Performance doesn’t guarantee future results. Annual returns were measured from December 31, 1977, to December 31, 2021. Equities are represented by the S&P 500 index. Fixed income is represented by the U.S. Aggregate Index

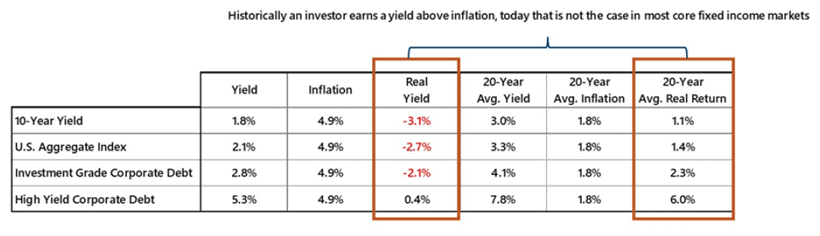

Fixed income’s historical behavior was driven by two primary forces, 1) interest rates have been in decline over much of the last four decades, which supported prices and 2) yields exceeded inflation, which helped to support purchasing power for goods and services. Today’s backdrop couldn’t be more different. Interest rates are moving higher as the U.S. Federal Reserve removes its accommodative stance and as seen in exhibit 2, yields are generally lower than inflation, creating a negative real yield environment.

Adding fuel to the proverbial fixed income fire, the average maturity of corporate bonds has lengthened considerably as corporations have taken advantage of low interest rates, issuing longer maturity bonds and locking in those low rates for years into the future. Longer maturities tend to have higher price volatility/sensitivity to moves up or down in interest rate; Duration is the technical term for this. In today’s world, this results in higher levels of price volatility within traditional fixed income portfolios.

Exhibit 2: Investors are getting negative real yields from fixed income, which hurts their purchasing power and limits the counterbalance performance behavior seen in Exhibit 1

Source: As of January 31, 2022. Past Performance doesn’t guarantee future results. Inflation is represented by the US Core Personal Consumption Expenditure “PCE” YoY change (as of 12/31/21). 10yr yield is represented by the yield from the 10-year U.S. government bond. U.S. Agg is represented by the U.S. Aggregate Bond index. Investment Grade Corp is represented by the Bloomberg US Corporate Bond Index. HY Corp is represented by Bloomberg US Corporate High Yield Bond index. Real yield = yield minus inflation

In our last quarterly commentary titled ‘Revving up their engines’ (January, 2022) we highlighted the need to consider unconstrained, opportunistic, non-traditional public fixed income, private credit and liquid alternatives as partial replacements or complements to traditional fixed income portfolios. These types of investments may offer lower price sensitivity during periods of rising interest rates and therefore may provide ingredients to enhance diversification, cash-flow as well as total return.

Private credit / direct lending can provide an attractive risk adjusted return and yield to the investor. With modest amounts of leverage, these strategies avoid the daily volatility experienced by their publicly traded peers and have little correlation to traditional credit markets.

Multi-sector bonds give an investor exposure to a broad opportunity set that can enhance overall income potential and diversify risk. Greater flexibility affords the manager the ability to pinpoint specific markets and sources of income to adapt to the market environment as conditions change.

Corporate high yield debt provides a greater yield than investment grade corporate credit but with a higher presumed default risk as well. Interestingly, companies falling into this category have been able to broadly shore up their balance sheets during the COVID-19 recovery resulting in limited defaults and attractive debt service ratios.

Market neutral strategies tend to appear in the “alternative” asset class but can exhibit a similar performance behavior as an investors’ non-traditional fixed income allocation. By using derivatives and convertible arbitrage, the strategies can have a wider scope of opportunities while enhancing diversification and providing downside protection during periods of market stress.

Albert Einstein once said, “the measure of intelligence is the ability to change.” We are living through unusual times where the traditional approach to fixed income investing needs to be broadened. At CWM, use the aforementioned strategies as ingredients to construct portfolios that exhibit a behavior capable of navigating this unusual period. As always, should you have any questions or would like to discuss how these strategies may contribute to your investment goals, please reach out to your Calamos Advisor or any member of your Advisory Team.

Past performance is not a guarantee or predictor of future results. Asset Allocation and Diversification does not guarantee a profit or protect against a loss. Capital market assumptions may be revised periodically, which can severely alter the results of different analyses. Calamos Wealth Management cannot give any assurances that these assumptions or any results relying upon these assumptions will prove correct. This information is not intended as a recommendation to invest in any particular asset class or as a promise of future performance. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve and should not be relied upon as recommendations to buy or sell securities. Assumptions, opinions and estimates are provided for illustrative purposes only. Forecasts of financial market trends that are based on current market conditions constitute our judgement and are subject to change without notice.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Calamos Wealth Management, LLC [“Calamos]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Calamos. Please remember to contact Calamos, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Calamos is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the Calamos’ current written disclosure brochure discussing our advisory services and fees continues to remain available upon request or at www.calamos.com.

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. The opinions and views of third parties do not represent the opinions or views of Calamos Wealth Management LLC. Opinions referenced are as of the date of publication and are subject to change due to changes in the market, economic conditions or changes in the legal and/or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

© 2022 Calamos Wealth Management. All Rights Reserved. Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.

CWM_2036586_0222O