Investment Insights Home Page

Quarterly Market Commentary - Q1 2024

Strong Start to 2024, but Risks Remain

April 9, 2024

The year 2024 has picked up right where 2023 left off, with strong performance across equity markets. The S&P 500 surged 10.6%, which outpaced the Nasdaq Composite Index of 9.3%. Themes that prevailed in 2023, like large cap over small cap and growth over value, continued their momentum in the first quarter. Russell 1000 Growth outperformed Russell 1000 Value broadly by about 2.4%, while large cap (Russell 1000) stocks outperformed small cap (Russell 2000) by over 5%.

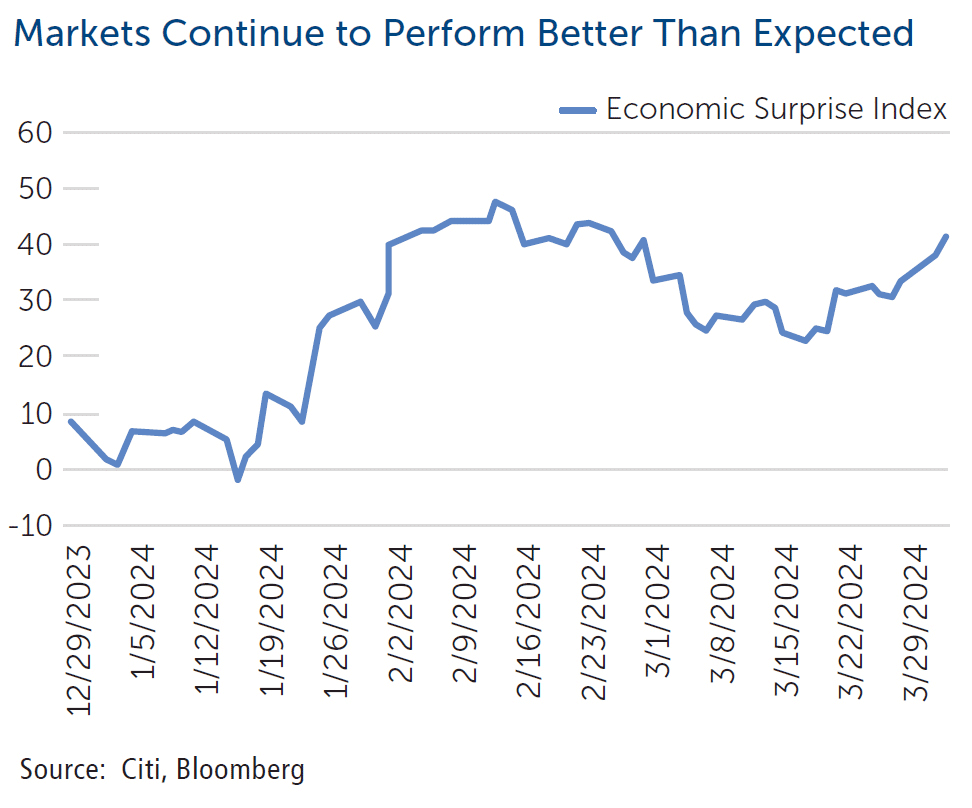

What is even more impressive about the continued equity rally is that it has occurred despite elevated geopolitical tensions and amid three major developed economies falling into recession (Germany, Japan and the United Kingdom). Still, markets have been focused on the incredible potential of Artificial Intelligence as well as the likely easing of US monetary policy later this year.

While we have been more optimistic than the market about the macro-outlook and probability of a “soft landing,” there are a number of risks that we remain focused on, including a policy error by the Federal Reserve; concerns about commercial real estate; geopolitical developments; and, of course, the US election this fall.

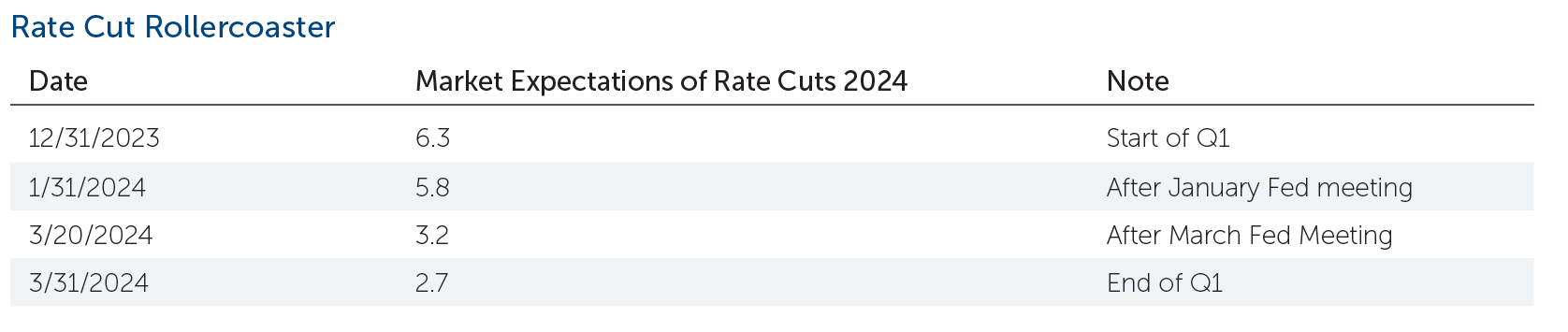

Will the Fed Get it Right?

Investors breathed a sigh of relief on March 20, when the US Federal Reserve confirmed their plan for three rate cuts this year. Because of a couple of higher than expected inflation prints to start the year, the market had been braced for the risk of the Fed waiting longer to reduce its policy rate. Along with the updated “dot plot,” the Fed also updated its forecasts for upward economic growth and inflation.

Market expectations for rate cuts have been on a wild ride this year, shifting from over six cuts priced in to begin the year to around three priced in currently, after falling to as low as 2.5. Importantly from our perspective, the market and the Fed are now aligned on rate projections.

While the Fed has been relatively successful thus far in lowering inflation without engineering a recession, dual-sided risks remain. The first risk is moving too slowly to reduce rates, negatively impacting the economy and risking recession. The second risk is easing too quickly, before clear evidence that inflation (and expectations for inflation) is falling toward the Fed’s 2% target.

A further consideration for the Fed is the upcoming US election We believe that Fed Chair Jerome Powell intends to begin any rates cuts well in advance of the election to avoid any perception of favoring one political party over the other. Recent stronger-than-expected economic data and inflation data complicates the landscape for the Fed.

While our base case remains that the Fed will cut rates two to three times this year, the start of any rate cuts may be pushed out until later this summer.

Commercial Real Estate Concerns

Concerns over banks’ exposure to commercial real estate have been in focus since last spring when three regional lenders failed. The latest news from New York Community Bancorp, which reported a surprise loss on January 31 and then a reported loss more than 10 times what it previously stated, led to the resignation of its CEO and rekindled some of the fears in the market. Shares of regional banks fell sharply after this latest development.

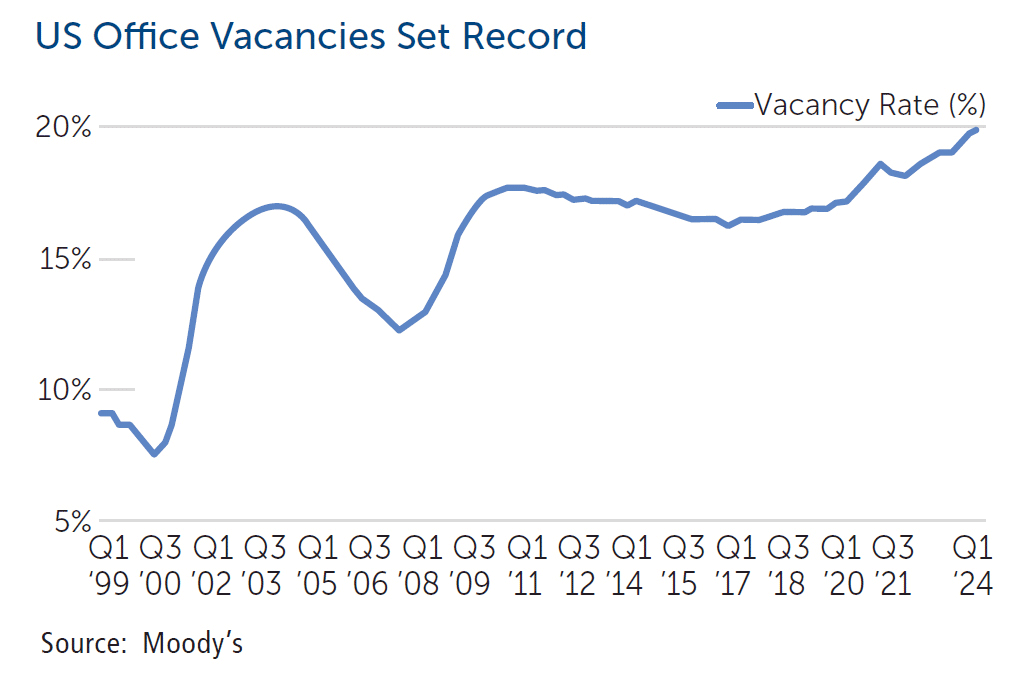

Further, the “extend and pretend” theme has continued in commercial real estate. Goldman Sachs estimated that $270bn of commercial mortgages expected to mature in 2023 have been extended into 2024. A good chunk of this debt pile origingated when interest rates were near zero, which means that borrowers will face a refinancing shock. Meanwhile, US office vacancies hit a fresh peak in the first quarter at nearly 20%, according to Moody’s.

Fed chair Jerome Powell said recently that commercial real estate’s impact on the banking sector is “a problem we’ll be working on for years.” This impact will likely be heavily felt by regional banks, given that they account for around 80% of all bank loans for commercial properties. Outside of regional banks, there is less concern. The Federal Reserve’s latest Financial Stability Report stated that “stress tests suggest the largest banks are well positioned to withstand a severe recession and contraction in CRE (Commercial Real Estate) markets.”

We do not expect the negative headlines around commercial real estate to go away anytime soon. However, we do not anticipate broader market contagion from this issue. In our real estate allocation to client portfolios, we are focused on areas like data centers and student housing where demand remains strong.

Geopolitical Considerations

As we noted, in our 2024 outlook, geopolitical risk remains elevated, because of ongoing Russia-Ukraine war as well as the Israel-Hamas war. On March 25, the U.N. Security Council passed a resolution demanding an immediate ceasefire.

Additionally, two years after Russia’s invasion of Ukraine, the situation remains extremely fluid regarding the Russia-Ukraine war. Russian President Putin recently escalated his rhetoric about the potential of Western troops fighting in Ukraine. The lack of clear “off ramps” clouds both of these situations and means that they will potentially be with us for some time.

Markets have climbed the “wall of worry” despite these increased geopolitical risks. We are closely watching areas such as commodity prices (in particular oil) and shipping costs to assess the outlook.

Geopolitical risks are by nature difficult to assess. While we continue to monitor developments in the Middle East as well as in the Russia-Ukraine war, we encourage our clients to remain fully invested in diversified portfolios.

While we are not overly bearish about any of these key risks, we are closely monitoring developments and stand ready to adjust tactical positioning as warranted. Please contact your wealth advisor for further details.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. The opinions and views of third parties do not represent the opinions or views of Calamos Wealth Management LLC. Opinions referenced are as of the date of publication and are subject to change due to changes in the market, economic conditions, or changes in the legal and/or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Calamos Wealth Management, LLC [“Calamos”]), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Calamos is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Calamos. Please remember that it remains your responsibility to advise Calamos, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request or at wm.calamos.com.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request.

S&P 500 Index is generally considered representative of the US stock market.

The Russell 2000 Index is comprised of the smallest 2000 companies in the Russell 3000 Index, representing approximately 8% of the Russell 3000 total market capitalization.

The Russell 1000 Index is a subset of the larger Russell 3000 Index and represents the 1000 top companies by market capitalization in the United States.

The Russell 1000 Growth and Value US ESG Indexes are alternatively-weighted US equity indexes based on the Russell US Style Indexes. The indexes are designed to meet improved index level ESG profile, while maintaining similar risk/return characteristics to the underlying universe.

The Bloomberg US Agg Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

CWM 822345 0424