Investment Insights Home Page

Market Spotlight: Will Powell's 'Skip' Turn into a 'Standstill'?

Jon Adams, Chief Investment Officer

June 14, 2023

With the Fed's decision to keep rates on hold at its June meeting, investors are understandably focused on what is coming next. Will this be a pause followed by one or more additional hikes, beginning as early as July? Or will it be difficult for the Fed to resume tightening once it has stopped?

Fed Chair Powell had telegraphed this pause in the weeks leading up to the meeting. Powell has been criticized for overcommunicating during this tightening cycle, leading to larger than usual fluctuations in investors' bets on future interest rate movements. We consider this to be a "hawkish" pause, as the new "dot plot" of policymaker expectations projects two additional hikes this year.

Immediately after the Fed meeting, markets were pricing in one additional rate hike in late July and, importantly, were no longer pricing in a rate cut in 2023. Significant cuts are priced in for the duration of 2024, though market expectations may prove too aggressive here.

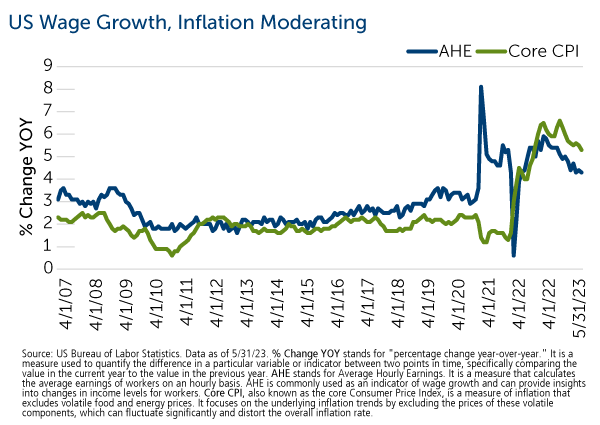

Tuesday's Consumer Price Inflation report showed that headline inflation rose by a lower than expected 4.0% year-over-year. This was the 11th consecutive decline in the inflation rate since it peaked at 8.9% last June and the lowest level since March 2021.

While fears of runaway inflation have abated, inflation is still running well above the Fed's 2% target, and more durable components of inflation like shelter costs remain uncomfortably high. The core CPI (which excludes food and energy) is running at 5.3% year-over-year.

One factor that is clear is that Federal Open Market Committee (FOMC) discussions will become more contentious given the divergence in outlook and different weighting on concerns about elevated inflation expectations becoming anchored on one side, and concerns about a potential recession and financial stability risks on the other side.

If the trajectory of inflation continues to slow, the Fed may not feel a need to tighten further, which would be welcomed by equity markets and risk assets more broadly. An end to rate hikes could be particularly supportive for US Growth and US Small Cap Equity. We stand ready to position portfolios for this scenario (and a potential soft landing), though we will be closely monitoring the economic backdrop.

Past performance may not be indicative of future results.

Consumer Price Inflation refers to the rate at which the general level of prices for goods and services is increasing, and subsequently, the purchasing power of currency is decreasing. It is commonly measured by tracking changes in a basket of goods and services over time, reflecting the average price increase experienced by consumers.

Core CPI also known as the core Consumer Price Index, is a measure of inflation that excludes volatile food and energy prices. It focuses on the underlying inflation trends by excluding the prices of these volatile components, which can fluctuate significantly and distort the overall inflation rate.

Federal Open Market Committee (FOMC) is a committee within the U.S. Federal Reserve System that is responsible for making monetary policy decisions. The FOMC meets regularly to assess the state of the economy, including factors such as inflation, employment, and economic growth, and determines the appropriate course of action for interest rates and other monetary policy tools.

US Growth refers to the economic expansion or growth of the United States. It typically refers to the increase in the country's Gross Domestic Product (GDP), which measures the total value of goods and services produced within a specific period. US Growth is an important indicator of the health and performance of the US economy.

US Small Cap Equity refers to investments in stocks or equity securities of small-cap companies in the United States. Small-cap companies generally have a smaller market capitalization compared to large-cap or mid-cap companies. Investing in US Small Cap Equity entails exposure to smaller companies with potentially higher growth prospects but also higher risks compared to larger and more established companies.

Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Calamos Wealth Management, LLC [“Calamos”]), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Calamos is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Calamos. Please remember that it remains your responsibility to advise Calamos, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request or at wm.calamos.com.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your accounts; and, (3) a description of each comparative benchmark/index is available upon request.

CWM 840419 0623