Advice & Planning Insights Home Page

The Grantor Retained Annuity Trust (GRAT)

November 6, 2019

Year-end tax planning discussions with wealthy clients are an opportune time to consider advanced gift planning techniques to transfer future appreciation of the family assets to the next generation, thus minimizing gift or estate tax consequences.

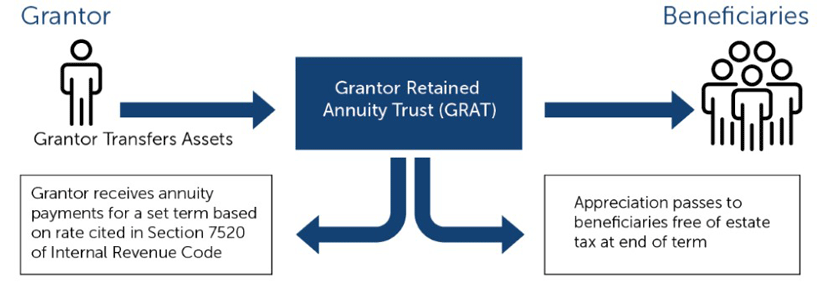

A grantor retained annuity trust is a trust arrangement created by a grantor interested in contributing assets with appreciation-potential to a fixed-term irrevocable trust. It is designed to freeze the current value of an asset while passing the appreciation of that asset onto non-charitable beneficiaries both free of gift and estate tax.

Here is the general structure: A Grantor creates an irrevocable trust for a certain term of years. The Grantor transfers assets into the trust and then an annuity stream and not the income of the trust is paid out to the Grantor every year. The IRS assumes that the trust assets will generate a return of at least the applicable interest rate cited in Section 7520 of the Internal Revenue Code in effect for the month the assets were transferred to the trust. Any appreciation in excess of the Section 7520 rate passes to the beneficiaries free of gift tax. (Section 7520 interest rates are available at www.irs.gov).

If the assets in the GRAT don’t outperform the Sec. 7520 rate, the assets are returned to the grantor at the end of the term. Specifically, the Grantor keeps the right to “retain,” over the term of the trust, the original value of assets plus an IRS-mandated interest rate. (Section 7520 of the Code)

The Grantor pays a tax when the trust is established (most planning is designed to reduce that tax to at or near zero). If the assets in the trust appreciate beyond a certain rate upon which the annuity is based, there will be assets in the trust after the term of the trust expires. When the trust expires the beneficiaries receive (tax-free) the assets left in the trust after the annuities to the Grantor are paid. These structures allow for the use of the estate tax exemption to be used for other purposes as, in most cases, no exemption is used in the creation of these trusts.

A GRAT does not qualify for the annual gift tax exclusion because the transfer is considered a gift of a future interest. Therefore, it is not a suitable estate planning tool to use in generation skipping transfer (GST), as the value of the skipped gift is not determined until the end of the trust term. The assets transferred to the beneficiaries will receive a carryover basis rather than a stepped-up basis. As such, higher basis assets are suitable assets for contributing to a GRAT.

From a gift tax perspective, the value distributed to the beneficiaries is excluded from the grantor’s estate, but the value of the annuity payments remains in the grantor’s estate.

In the simplest terms, at the end of a GRAT term, if a Grantor contributes $20mm into a GRAT and it grows to $30mm, after the end of the term, $20mm plus the 7520 rate of interest will be retained by the Grantor and $10mm of growth minus the 7520 rate of interest will be received by the beneficiaries. With interest rates (including the 7520 rate) at generational lows, this technique is a popular tool in most estate planners’ arsenals.

If the Grantor dies before the term of the trust expires, the assets of the trust are included in the Grantor’s estate. Many GRATS are designed to have short terms to reduce the likelihood of this event, or the grantor can make provisions to pass the right to receive any remaining annuity payments to the surviving spouse through a marital trust and qualify for the estate tax marital deduction, which could eliminate any estate tax liability relating to the GRAT assets.

A GRAT will be treated as a grantor trust for principal and income purposes allowing some additional income benefits to the grantor and beneficiaries. As a Grantor trust, all income, gains, losses and credits will be taxed to the grantor. In addition, a grantor trust may be an S corporation shareholder.

GRATs are particularly flexible structures and can provide beneficiaries with a higher value of assets at the end of the term by increasing the annuity payment by up to 20% per year (under Regs. Sec. 25.2702-03(b)(1). This means that the grantor can receive smaller annuity payments in the early years of the GRAT term, leaving more assets in the GRAT to appreciate during the term of the GRAT.

Annuity payments can come in the form of interest or as a percentage of the overall value of the assets. They can be in the form of cash, shares or units of a business. When combined with minority and liquidity discount reduction strategies, GRATs can be particularly effective in transferring appreciated asset value to their beneficiaries. The GRAT beneficiaries can be new trusts arrangements instead of individual beneficiaries

These receiving trusts can be new “rolling” GRATs to create a long term plan for asset transfer that reduces the negative effects of price volatility. While diversification is a common thread in an investment plan, concentration actually is a better strategy for GRATs as there is great potential upside if the assets appreciate quickly, yet very little downside if they do fail to cross the 7520 hurdle. Those assets just revert back to the Grantor in the annuity payment and the process can be attempted again with no penalty.

Popular assets in GRATs include Family Limited Partnerships (including the use of discounting techniques to amplify the strategy’s effectiveness), hedge fund interests, real estate, stock portfolios and single stock positions and other high growth potential assets. Additionally, properly structured GRATs can be shareholders in S corporations, so closely held business interests may be contributed to a GRAT.

GRATs continue to grow in numbers among wealthy families’ estate plans. They are attractive intra-family wealth transfer tools with little to no gift tax cost. As a result, several legislative proposals have been on review to increase the minimum term of 10 years and a residual value greater than zero. Now may be the time to take advantage of the current GRAT-friendly environment and transfer appreciation to beneficiaries and take advantage of low interest rates.

Calamos Wealth Management and its representatives do not provide accounting, tax or legal advice. Each individual’s tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation. For more information about federal and state taxes, please consult the Internal Revenue Service and the appropriate state-level departments of revenue, respectively. This material is provided for informational purposes only and should not be considered tax or legal advice. The views and strategies described may not be suitable for all investors.

You should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized advice from Calamos Wealth Management LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Calamos Wealth Management LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Calamos Wealth Management LLC client, please remember to contact Calamos Wealth Management LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Calamos Wealth Management LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.