Advice & Planning Insights Home Page

Spousal Lifetime Access Trusts (SLATs)

December 5, 2019

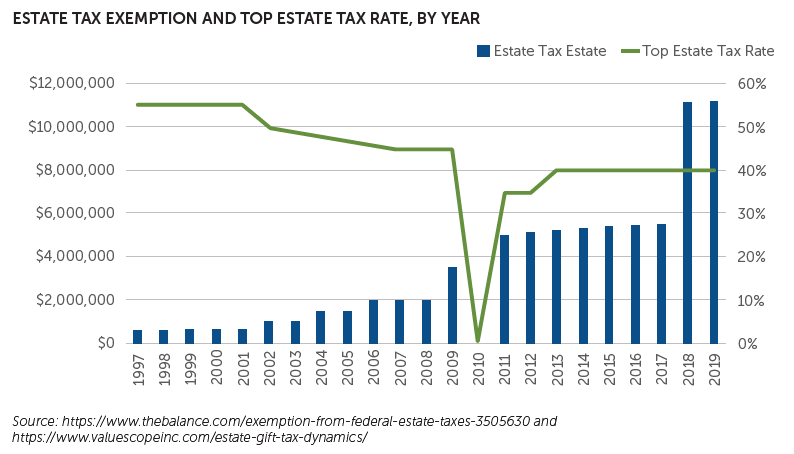

The 2019 federal estate tax exemption is a robust $11,400,000, but pitfalls and politics remain important to be aware of. For example:

- The current federal estate tax exemption sunsets in 2025. Under current law, the level will revert to the 2017 level of $5,490,000. That figure could potentially be lowered by a future Congress and president.

- State laws and tax regimes do not necessarily align with federal estate tax exemptions, potentially leading to substantial taxes due—some or all of which might be avoidable with prudent financial planning.

The current estate-tax environment is about as favorable as it’s ever been (see figure above). Of course, it’s possible that a future Congress will make these provisions yet more favorable. But in our view, to ignore the risk of a return to more historically familiar levels is a mistake.

With interest rates at generationally low levels, this is a good time to review one’s estate plan to ensure that it squares with the current tax and legal environment and takes advantage of market conditions.

As 2020 comes into view, a popular estate planning tactic, the SLAT, is receiving attention from estate planners as they advise their clients on the current environment and the potentially shifting landscape. Spousal lifetime access trusts (SLATs) are a flexible estate planning tool that potentially provides families with the opportunity to provide structure and stability around their wealth.

What is a SLAT?

A Spousal Lifetime Access Trust (“SLAT”) is an irrevocable trust created by one spouse for the benefit of the other. Other family members, including children and/or grandchildren can benefit as well. The grantor, or “donor spouse,” uses their gift tax exemption to make a gift to the SLAT, and the “beneficiary spouse” is named as a current beneficiary.

While the donor spouse gives up his or her right to the property transferred into the trust, the beneficiary spouse maintains access to that same property. Drafters of these trusts have a lot of flexibility in structuring the trusts depending on the clients’ needs.

For example, the trust can be drafted to allow only the beneficiary spouse to access funds during his or her lifetime, while children and grandchildren benefit after the beneficiary spouse’s death. Or, drafters could design SLATs to permit distributions to the beneficiary spouse and children at the same time.

Positive Tax Considerations in the Current Regime

The 2019 estate and gift tax exemption of $11,400,000 per individual can be used during life or at death. It does not need to be used all at once. When structured correctly, these assets and their future value fall outside of the estate tax regime. The exemption can be used with a variety of different assets (both liquid and illiquid).

In order to increase the after-tax effectiveness of an asset transfer, it is common practice to use assets that have the potential to appreciate significantly. Assets that are not paid out to the beneficiary spouse remain in the trust and may continue to grow free of estate and gift taxes while remaining available for the next generation. Thus, a SLAT can be both an effective wealth structuring tool and a good estate tax planning vehicle.

SLATs are taxed as grantor trusts for income tax purposes. This means that the “donor spouse” bears the income tax burden of the trust. Many planners view this as a way to enhance the effectiveness of the trust as an estate planning vehicle. By allowing the trust to grow without the drag of income taxes (as they are being paid by the grantor), more of the assets can flow to the next generation. Additionally, the grantor’s payment of these taxes is not an additional gift for transfer tax purposes.

Factors to Consider

A SLAT is one of many transfer planning techniques that can be used within one’s estate plan. It is not a cure-all or magic pill and needs to be employed within the context of an overall discussion of estate planning goals and desires. Like most structures, if constructed in haste, it can frustrate one’s ultimate goals.

Here are some things to think about in using a SLAT in one’s estate plan.

- Irrevocable Trust.The transfer must be a completed gift which means that grantor cannot retain a beneficial interest in the trust. On the positive side, the SLAT will not be included in the grantor’s estate.

- Choice of trustee.The donor spouse should not serve as trustee. A beneficiary spouse may serve as a trustee, but only so long as the power to make distributions to him or herself is restricted by an ascertainable standard which would be defined in the trust. It is standard practice to have the spouses or beneficiaries have the power to change or remove trustees. In some cases, a corporate trustee or co-trustee may be appropriate.

- The primary beneficiary is the beneficiary spouse. Children, grandchildren and other descendants may also be named as either current or remainder beneficiaries.

- Many types of assets can be used in a SLAT. Especially for those who rely on SLAT assets for current income needs, a thoughtful allocation of assets within the portfolio is necessary to ensure that the need for income is balanced with the growth potential and that the estate tax effectiveness of the SLAT is maintained. Borrowing against the assets in a SLAT is possible if properly drafted.

- The Impact of Joint Property. As previously discussed, a SLAT can be funded with a variety of assets. However, it is important for the donor spouse NOT to fund the SLAT with assets jointly owned with the beneficiary spouse. Using joint property could taint the trust by creating the appearance that the beneficiary spouse is making the gift to the trust. This would reduce the effectiveness of the transfer planning.

- Asymmetrical Language in Dual Trusts. For those families where each spouse may be using SLATs for the benefit of the other as part of overall planning, there needs to be tangible difference in terms between the trusts. If not dissimilar enough, the two trusts could be taken together by the IRS and the positive estate planning tax impacts reduced. Particular care must be taken in drafting to ensure that this risk is minimized.

- A SLAT is probably not a good idea in difficult marital situations. Good practice dictates that any estate planning done with a spouse be coordinated with any marital agreements that have been put in place. A SLAT works when the estate planning and marital income needs are aligned and coordinated. Divorce would have the effect of cutting off a donor spouse’s indirect access to the SLAT’s assets. Without proper attention to detail, the trust can also result in the continued support of an estranged spouse. One way to defend against this is to structure the SLAT so it is available only for any current spouse (and not former or estranged spouses). The SLAT can also be drafted to eliminate a spousal beneficiary completely in the event of divorce. Finally, in community property states, the community nature of assets contributed to the trust must also be taken into account and likely severed.

As the political climate continues to sort itself out with the approach of the 2020 elections, the conditions for effective estate planning continue to be positive. SLATs are still popular vehicles among estate planners and a useful tool for clients to consider as they review their estate plans for the future.

Calamos Wealth Management and its representatives do not provide accounting, tax or legal advice. Each individual’s tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation. For more information about federal and state taxes, please consult the Internal Revenue Service and the appropriate state-level departments of revenue, respectively. Any estate plan should be prepared and reviewed by an attorney who specializes in estate planning and is licensed to practice estate law in your state.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. You should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized advice from Calamos Wealth Management LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Calamos Wealth Management LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Calamos Wealth Management LLC client, please remember to contact Calamos Wealth Management LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Calamos Wealth Management LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.