Advice & Planning Insights Home Page

Potential Tax Savings Through Cash Balance Pension Plans

February 6, 2024

Many business owners and entrepreneurs are seeking ways to maximize their retirement plan savings. Cash balance pension plans soared in popularity in response to those needs—and thanks to clearer guidance issued by the IRS in 2010.

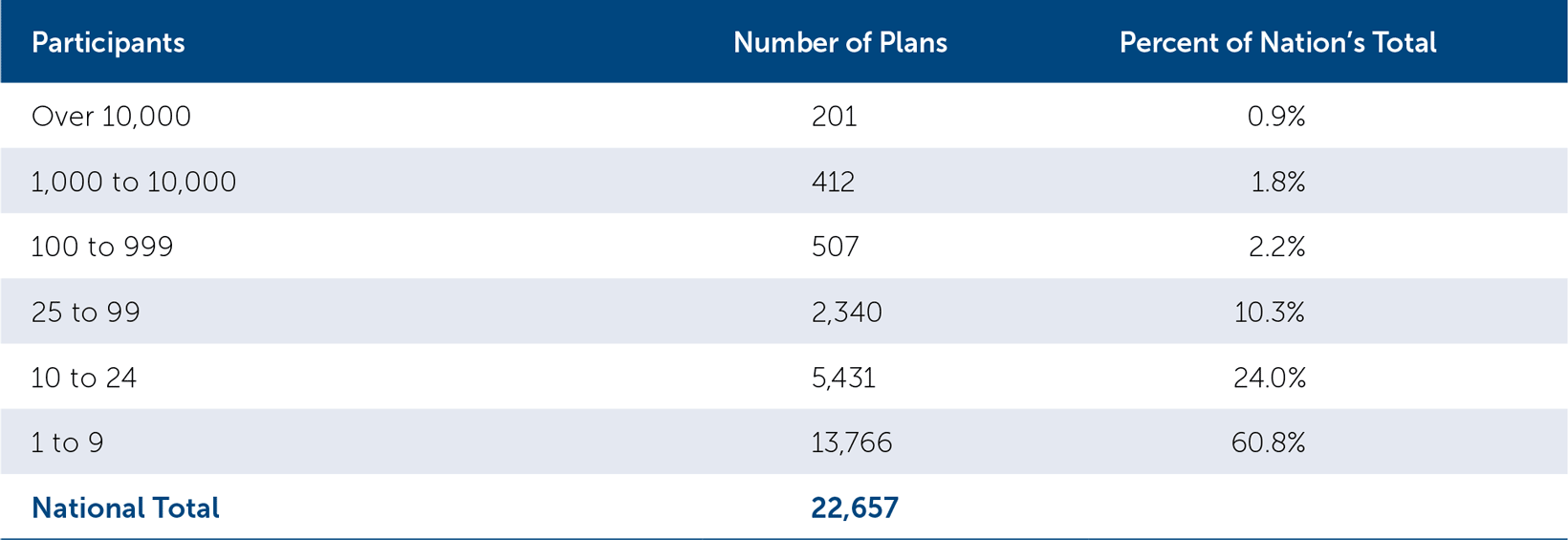

Specifically, the period 2002-2020 saw a fifteen-fold increase in new cash balance pension funds, according to the 2023 National Cash Balance Research Report, presented by FuturePlan Cash Balance Center of Excellence. Also, based on analysis performed by FuturePlan, using 2020 data from IRS Form 5500 filings (the most current data available), the March 2023 National Cash Balance Research Report noted that there were 22,657 cash balance plans covering more than 9.3 million participants, with assets of $1.2 trillion.

Here’s more context for their growth in popularity, also from the report’s findings:

- The number of new cash balance plans increased 6% from 2019 to 2020, compared with just 3% growth in new 401(k) plans.

- Cash balance plan sponsors contributed $24.3B in 2020.

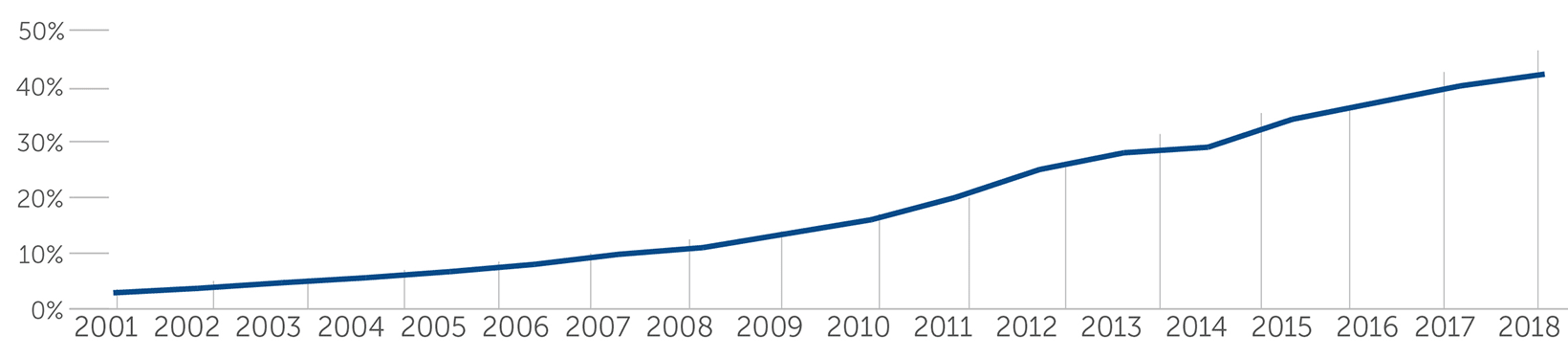

Cash Balance plans represented more then 37% of all defined benefit plans in 2018 versus only 3% in 2001

Source: 2023 National Cash Balance Research Report, FuturePlan

So who’s using cash balance pension plans?

While some Fortune 500 companies have converted their traditional pension plans to a cash balance format, small and medium-sized businesses have contributed most to the recent popularity of these plans. These plans are ideally suited for businesses that have consistent cash flow and are highly profitable.

Companies with 100 employees or less now represent 95% of all cash balance pension plans, and nearly 61% of all cash balance plans are sponsored by employers with fewer than 10 employees.

What exactly is a cash balance plan?

First introduced in the mid-1980s, these plans were used sparingly and didn’t catch on until certain legal issues were clarified in the 2006 Pension Protection Act, 2010 IRS Cash Balance regulations, 2014 Final IRS Cash Balance regulations, 2017 Tax Cuts and Jobs Act* and 2019 SECURE Act 1.0.

Cash balance pension plans are employer-sponsored retirement plans that incorporate elements from traditional defined benefit plans along with the flexible characteristics of defined contribution plans (401k). These hybrid plans provide the ability for high income business owners and partners in professional service firms to save upwards of $266,000 annually based upon demographics and plan design**.

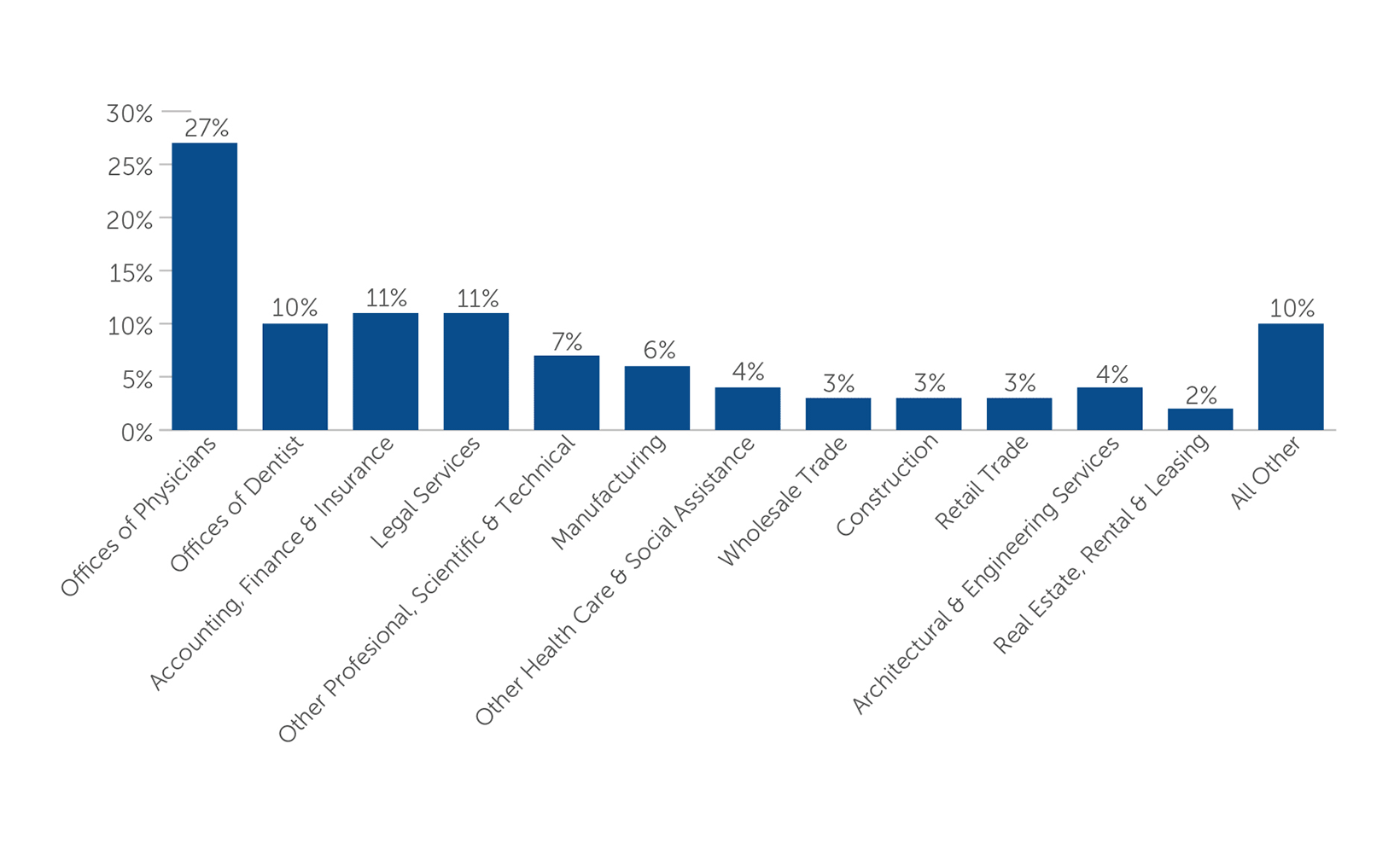

48% of all plans are sponsored by medical/dental groups and law firms

Source: Kravitz 2018 National Cash Balance Research Report.

Similar to traditional defined benefit plans, employers make contributions for the benefit of each employee. However, instead of using an actuarial rate of return, the employer makes two contributions for each employee. The first is a pay credit, which is either a fixed amount or a percentage of annual compensation. The second contribution is an interest credit rate (ICR) which is typically set to equal the actual rate of return of the portfolio, thereby reducing the investment risk of market volatility and the possibility of having an underfunded plan.

Another defining difference is that a hypothetical account is maintained for each employee. Contributions are recorded into these accounts, providing the employee with the ability to understand their benefit as a hypothetical account balance, similar to a 401(k) account, instead of a specific monthly benefit upon retirement.

To maximize their effectiveness, 96% of cash balance pension plans are combined with 401(k), profit sharing and other defined contribution plans. This allows for plans that are maximized for the benefit of the business owner while also helping to recruit and retain employees.

Benefits of cash balance pension plans

- Not all participants are equal – plans can be designed to maximize benefits to owners, while minimizing contributions to other employees. Since contributions are age-based, older business owners may be able to contribute as much as $266,000 annually and reap upwards of 90% of the benefits of the plan*.

- Income tax reduction strategies – contributions to retirement plans reduce your taxable income dollar for dollar. With a 37% current maximum Federal tax rate (scheduled to increase to 39.6% after expiration on December 31, 2025, of the Tax Cuts & Jobs Act of 2017), along with additional taxes on earned income over $200,000 ($250,000 married, filing jointly) for Medicare and Obamacare surcharges, the income tax savings for high-income earners could be significant for participants in a cash balance pension plan.

- Asset protection – all qualified pension plans are protected under the Employee Retirement Income Security Act of 1974 (ERISA). The ability to accumulate large sums makes these plans particularly attractive to doctors, lawyers, and entrepreneurs.

- Eliminate the potential of an underfunded pension liability – regulatory revisions allow the plan’s ICR to equal the plan’s actual rate of return, thereby eliminating a plan’s ability to be underfunded due to market declines. The plan’s assets must be adequately diversified.

- Federal guarantee – as with all pension plans, cash balance plans can be guaranteed by the Pension Benefit Guaranty Corporation for a nominal fee.

- Portability and value – IRS regulation allows for a maximum accumulation of $3.4 million. After a 3-year vesting period, account values can be rolled over to an Individual Retirement Account (IRA) or a lifetime annuity can be purchased. Knowing the market value of your retirement benefit makes planning more meaningful and easier to understand.

Is a cash balance plan right for you?

Cash balance pension plans represent an opportunity for business owners to take advantage of enhanced tax savings, maximizing their retirement savings and protecting their assets. They have changed the landscape of retirement planning, especially as their popularity has soared.

Because all qualified retirement plans are subject to a myriad of regulatory issues, we recommend engaging a qualified third-party actuary to design a plan to meet your needs.

*Provision 11011 SEction 199A of the 2017 Tax Cuts and Jobs Act.

**2023 age-based contribution limit for 57 year old participant. Contribution amounts vary, based on factors including, but not limited to: age, interest rates & mortality tables. Actual contribution amounts are determined by an actuary.

Calamos Wealth Management and its representatives do not provide accounting, tax or legal advice. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Each individual’s tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation. For more information about federal and state taxes, please consult the Internal Revenue Service and the appropriate state-level departments of revenue, respectively. This information is provided for informational purposes only and should not be considered tax or legal advice.

You should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized advice from Calamos Wealth Management LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Calamos Wealth Management LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Calamos Wealth Management LLC client, please remember to contact Calamos Wealth Management LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Calamos Wealth Management LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.